Details of the proposed changes regarding sanctioning of responsible individuals.

Historically the Audit Registration Committee (ARC) has applied regulatory penalties and restrictions to firms only, and not responsible individuals (RIs). The only options currently available to the ARC in relation to an RI’s actions are removal of RI status or referral of the matter to the Conduct Department for a disciplinary investigation.

However, there is an implicit requirement in the FRC delegation agreement for the powers of the FRC set out in SATCAR3 to be mirrored in those of the RSBs, and as the FRC often apply penalties restrictions and suspensions to RIs as well as firms, this is a power which should be clearly recognised by RSBs in the Audit Regulations.

In addition, the new requirements emerging on CPD where the responsibility falls equally on firm and individual require that the individual as well as the firm is held to account through the sanctions available. It would be disproportionate and ill-targeted to pass through to the Conduct Committee minor infractions by an individual relating to CPD which could be dealt swiftly by the ARC rather than draw out over the longer disciplinary process.

It is therefore proposed that the Audit Regulations are updated to include the ability for the ARC to issue regulatory penalties and impose restrictions on RIs as well as firms. The ARC’s current powers would also remain available.

It should be noted that in most cases the ARC will focus enforcement action on the firm and leave the firm to apply its own enforcement processes to relevant responsible individuals. However, the FRC expect the ARC to exercise this power where circumstances warrant it.

3 Statutory Auditors and Third Country Auditor Regulations 2016

Regulatory changes – sanctioning of responsible Individuals

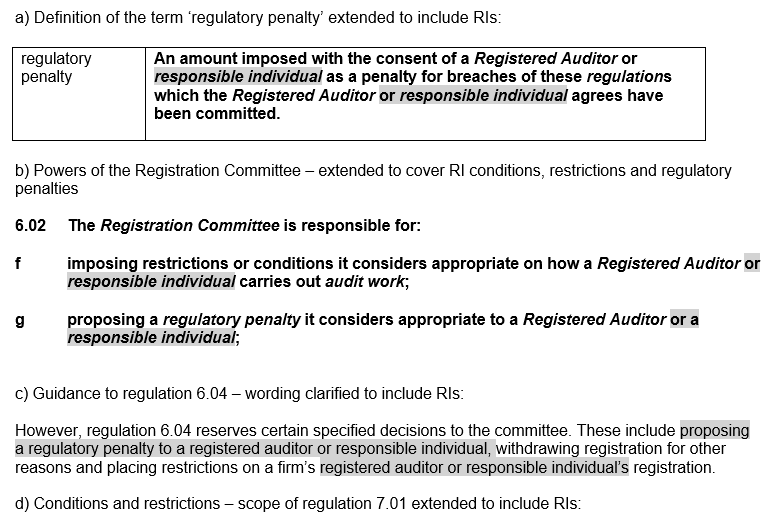

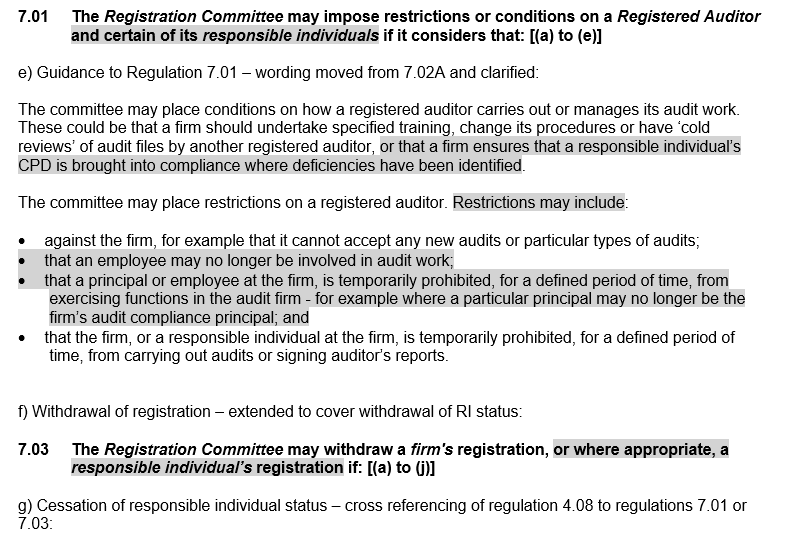

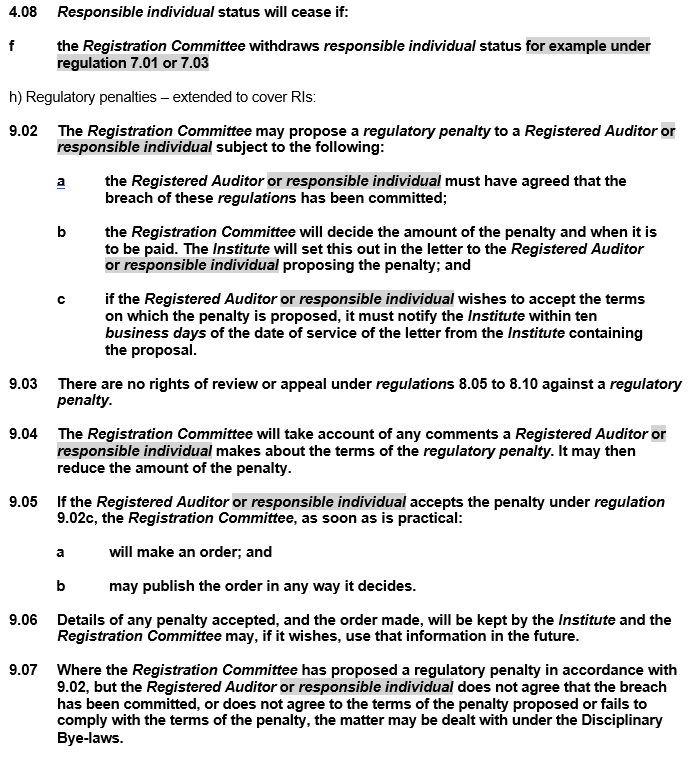

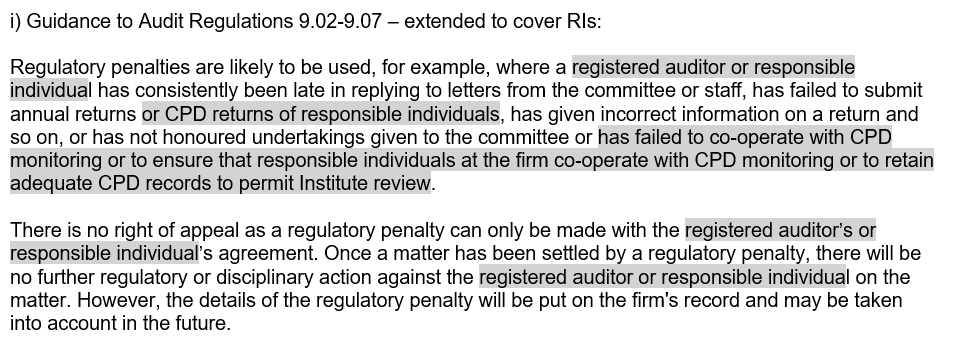

The following changes are proposed to the Audit Regulations (additions are highlighted in grey in the images provided):

Questions 10-11 (of 12, in total)

- Are the proposed revisions in the Audit Regulations regarding sanctioning of responsible individuals sufficiently clear?

- Are there any practical difficulties in achieving the obligations set out in these revisions?