The latest national Business Confidence Monitor (BCM) shows that business sentiment was on course to move into positive territory in Q1 2026, but the outbreak of the Iran war had a dramatic impact in the final weeks of the survey period, with confidence deteriorating sharply. While businesses reported improved annual domestic sales and exports growth and easing input price inflation compared with Q4 2025, the war introduced significant downside risks to the outlook for the coming year.

Key points

- The Business Confidence Index was rising in Q1 2026 but sentiment fell sharply at the end of the survey period following the outbreak of the Iran war and the overall Q1 score remains in negative territory at -1.1, the fifth consecutive negative quarterly score.

- Annual domestic sales and exports growth rose and companies were optimistic about both for the coming year, however expectations deteriorated at the end of the survey period as the impact of the conflict took hold.

- Inflationary pressures are likely to mount despite a slowdown in annual input price inflation reported in Q1 2026. Labour costs were the most widely reported growing challenge amid rising wage growth, while more than a third of businesses flagged energy prices as oil and gas volatility picked up.

- Concerns about the tax burden eased from the survey historical high recorded last quarter but remain almost three-times the historical norm, while regulatory concerns remain elevated.

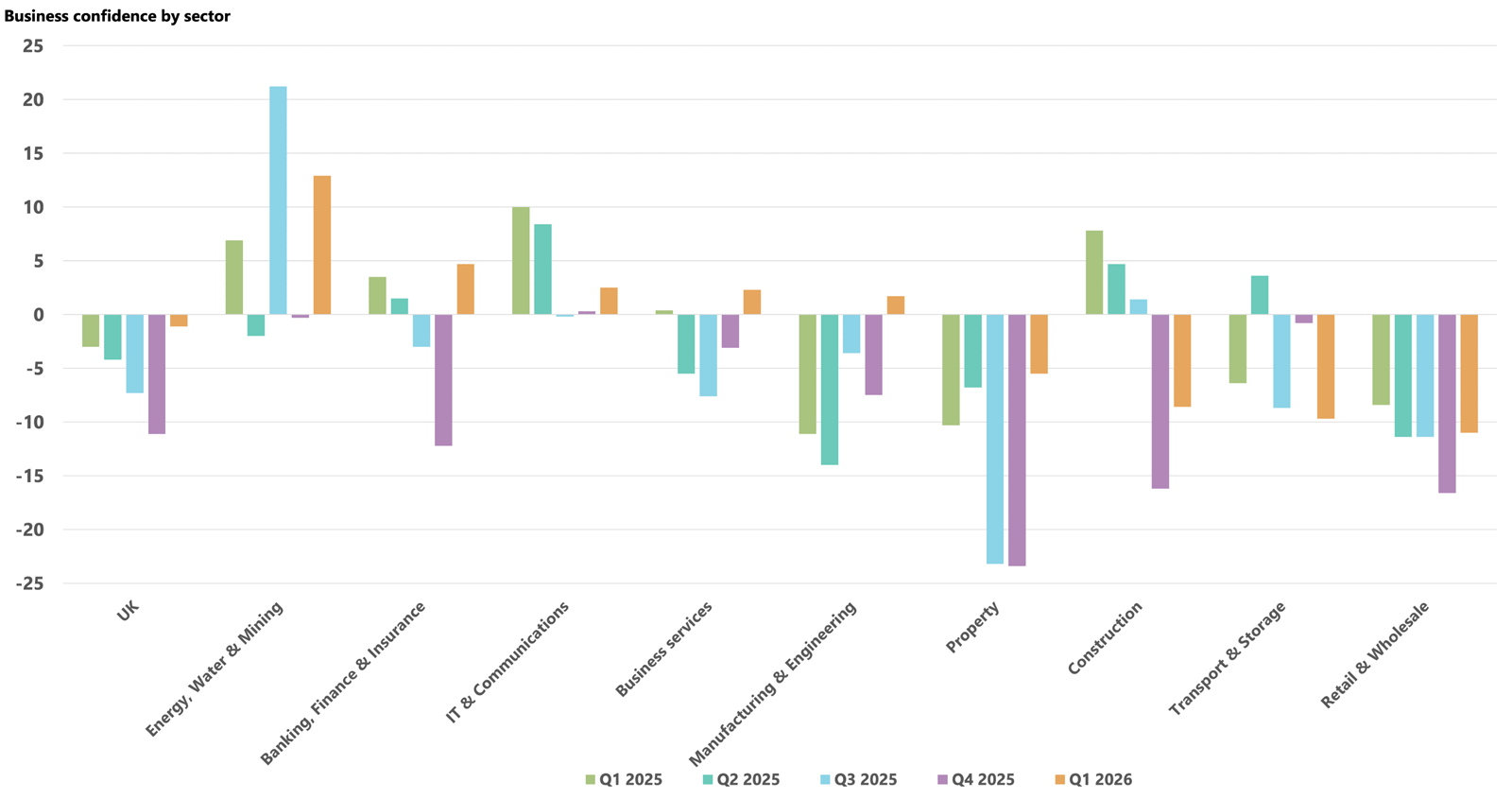

- Confidence improved in most sectors though scores vary widely. Sentiment is highest and in positive territory in Energy, Water & Mining, Banking, Finance & Insurance and IT & Communications but is deeply negative in Retail & Wholesale, Transport & Storage and Construction.

Confidence overall

Middle East conflict curbs rise in UK business confidence

- Business confidence was recovering in Q1 2026 but sentiment fell following the outbreak of the Iran war and the overall Q1 score remains in negative territory.

- The improvement in confidence was underpinned by strengthening domestic and export sales growth but expectations were dented by the Middle East conflict.

- Sentiment improved in most sectors over the quarter, and is highest in Energy, Water & Mining, IT & Communications and Business Services and lowest in Retail & Wholesale, Transport & Storage and Construction.

Business confidence was improving over the survey period but sentiment has fallen sharply since the outbreak of the Iran war on 28 February. Survey results for the period up to 3 March show that confidence had moved into positive territory but fell back sharply in the following weeks, dragging the overall Q1 score down to -1.1. Though sentiment has improved from the reading of -11.1 in Q4 2025, the impact of the Iran war means confidence has now been in negative territory for five successive quarters, the longest period since Q2 2018 to Q3 2019.

Improved sales underpinned the rise in confidence, with domestic sales expanding by 3.5% in the year to Q1 2026 and rising above the historical norm (3.1%). Companies also reported improved annual exports sales growth in the quarter, at 3.3%, and above the historical average (3.0%) for the first time since Q3 2023. Businesses were increasingly upbeat about sales prospects, expecting domestic sales growth to rise to 5.4% over the coming year and exports growth to rise to 4.1%. However, the conflict in the Middle East dented these expectations and the risks to the outlook are weighted on the downside.

Confidence improved in most sectors in the quarter though scores are highly uneven. Energy, Water & Mining is most positive (+12.9), followed by Banking, Finance & Insurance (+4.7) and IT & Communications (+2.5). Manufacturing (+1.7) also edged into positive territory for the first time since Q4 2024, though weekly survey data shows sentiment in the sector was heavily impacted by the Iran war. Retail & Wholesaling (-11.0) is now the most pessimistic sector having recorded its sixth consecutive negative score. Construction (-8.6) also remains among the least optimistic sectors, despite a sharp improvement from last quarter. Transport & Storage (-9.7) was the only sector to record a decline in confidence.

Business challenges

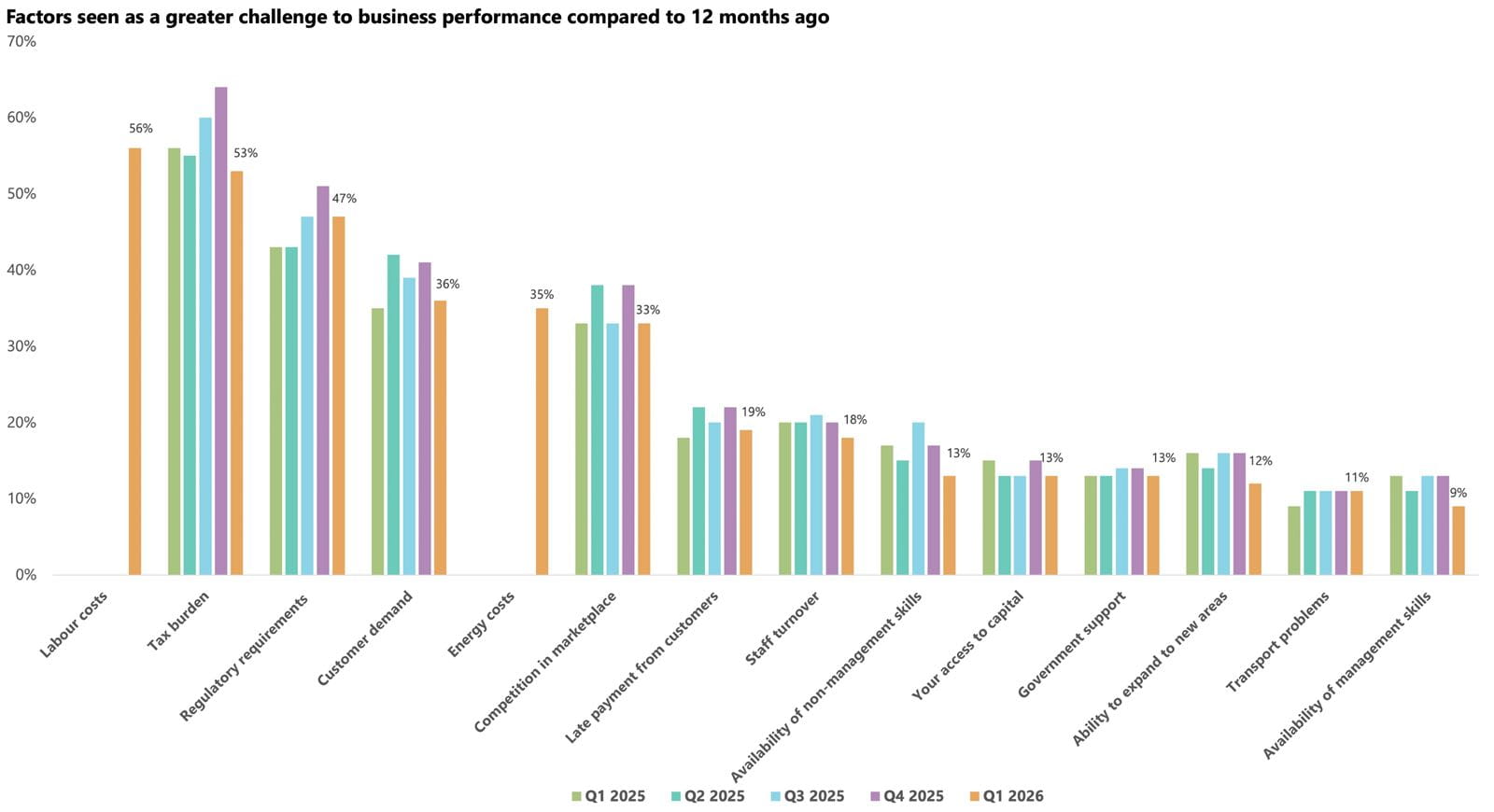

Labour and energy costs join the tax burden and customer demand among the most widespread growing challenges facing businesses

- Labour costs are the most widespread growing challenge in Q1 2026 as tax concerns eased back from their historical high recorded in Q4 2025.

- Energy costs were reported by over a third of companies as cost pressures related to the Iran war are likely to rise.

- Regulatory concerns remain above their historical norm, while customer demand has dipped below the average.

Over half (56%) of companies surveyed reported labour costs as a growing challenge, the most widely cited challenge in Q1 2026. This was the first time the challenge was included in the survey, with the high proportion likely reflecting the previous rise in employers’ National Insurance Contributions, the April 2026 increase in the National Living Wage and concerns around potential additional costs linked to the Employee Rights Act. This issue was particularly marked for labour-intensive sectors including Retail & Wholesale (69%) and Construction (67%).

Concern about the tax burden eased to 53% from the survey high of 64% recorded last quarter, but the proportion remains close to three-times the historical average (19%). Once again, reports about the tax burden were most prevalent among Construction (66%) and Retail & Wholesale (61%) businesses.

Companies were also asked about energy costs as a growing challenge for the first time in the survey and over a third (35%) reported the issue, with the challenge likely to become more prevalent due to the ongoing uncertainty surrounding oil and gas prices linked to the Middle East conflict. The issue was flagged by 44% of Transport & Storage businesses and 43% of Energy, Water & Mining companies. Two-fifths (40%) of Retailers and Property companies also cited the issue as a growing concern.

Regulatory requirements edged down compared to last quarter but with the issue reported by 47% of companies in Q1 2026, it remains above the historical survey average (40%). Regulatory concerns rose in Construction to a new survey record high (58%), while it remained elevated in Property (54%), Energy, Water & Mining (53%) and Retail & Wholesale (50%).

Concerns about customer demand (36%) also eased, dropping below the historical norm (38%). Over half of Construction businesses (51%) reported the issue, the highest of all sectors in Q1 2026, with the proportion rising from the previous quarter. After reaching a near survey high of 61% in Retail & Wholesale in Q4 2025, the proportion fell back to 47% this quarter but remains around the historical sector norm (44%).

Prices

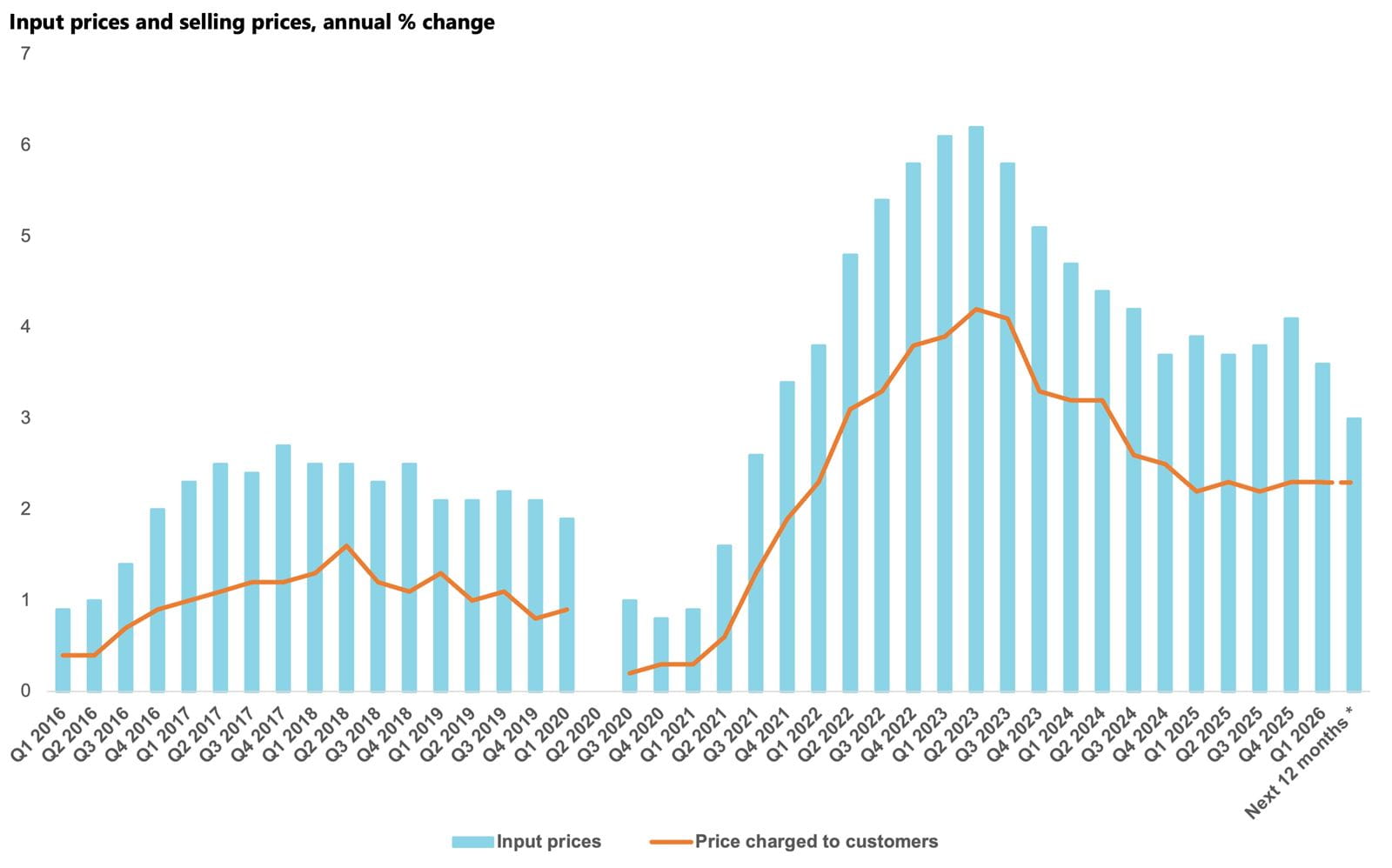

Annual input price inflation eased in Q1 2026 but Iran war poses significant risks to the outlook

- Annual input price inflation eased in Q1 2026 compared with the previous quarter, with further moderation expected, but the Iran conflict poses a significant risk to these projections.

- Selling price inflation was flat compared to the previous quarter and companies plan to keep this pace over the next 12 months, though rising input costs could push prices higher.

- Most sectors expect softer input inflation but Property, Transport & Storage, and Energy, Water & Mining foresee marked selling price increases compared to last year.

After rising in each of the two previous quarters, annual input price inflation eased from 4.1% in Q4 2025 to 3.6% in Q1 2026, the smallest increase since Q4 2021. The latest official data show that annual CPI inflation moved closer to the Bank of England’s 2.0% target in recent months, declining to 3.0% in the year to February. The announcement that the Ofgem energy price cap will be cut by 6.6% in April 2026 likely supported expectations that annual input inflation would moderate further in the year ahead, with businesses anticipating growth of 3.0% y/y, just marginally above the 2.7% historical average. However, since the closure of the Strait of Hormuz on 2 March, oil and gas prices have spiked, posing a major risk to these forecasts. While the government has announced measures to support households, businesses have been left exposed to higher energy costs.

All sectors reported that annual input cost growth slowed in the year to Q1 2026, with the smallest increases observed in Banking, Finance & Insurance (2.7%), Transport & Storage (3.1%) and Energy, Water & Mining (3.1%), though rates in all three were still above their respective historical averages. Most sectors expected input price inflation to soften further in the year ahead, although these projections were largely established before the escalation of the conflict in the Middle East and are likely to have changed in recent weeks. Banking, Finance & Insurance anticipated the smallest increase, at just 2.3%, while companies in the Business Services sector projected the highest rate over the next 12 months, at 3.3%.

Businesses maintained the rate at which they increased their selling prices at 2.3% in the year to Q1 2026, above the historical norm of 1.4%, and expect to continue increasing their prices at this pace over the year ahead, though higher input cost inflation is likely to put upward pressure on selling prices.

In Q1 2026, most sectors slowed the rate at which they raised their selling prices compared with the previous quarter. Business Services and Manufacturing and Engineering were the greatest exceptions to this trend, with companies in these sectors raising their prices by 3.1% and 2.9%, respectively. Looking ahead, Transport & Storage and Energy, Water & Mining ‒ the sectors most exposed to the spike in energy prices ‒ plan to increase their selling prices sharply over the coming year, with anticipated rises of 2.9% and 2.8%, significantly above their respective historical norms.

Employment

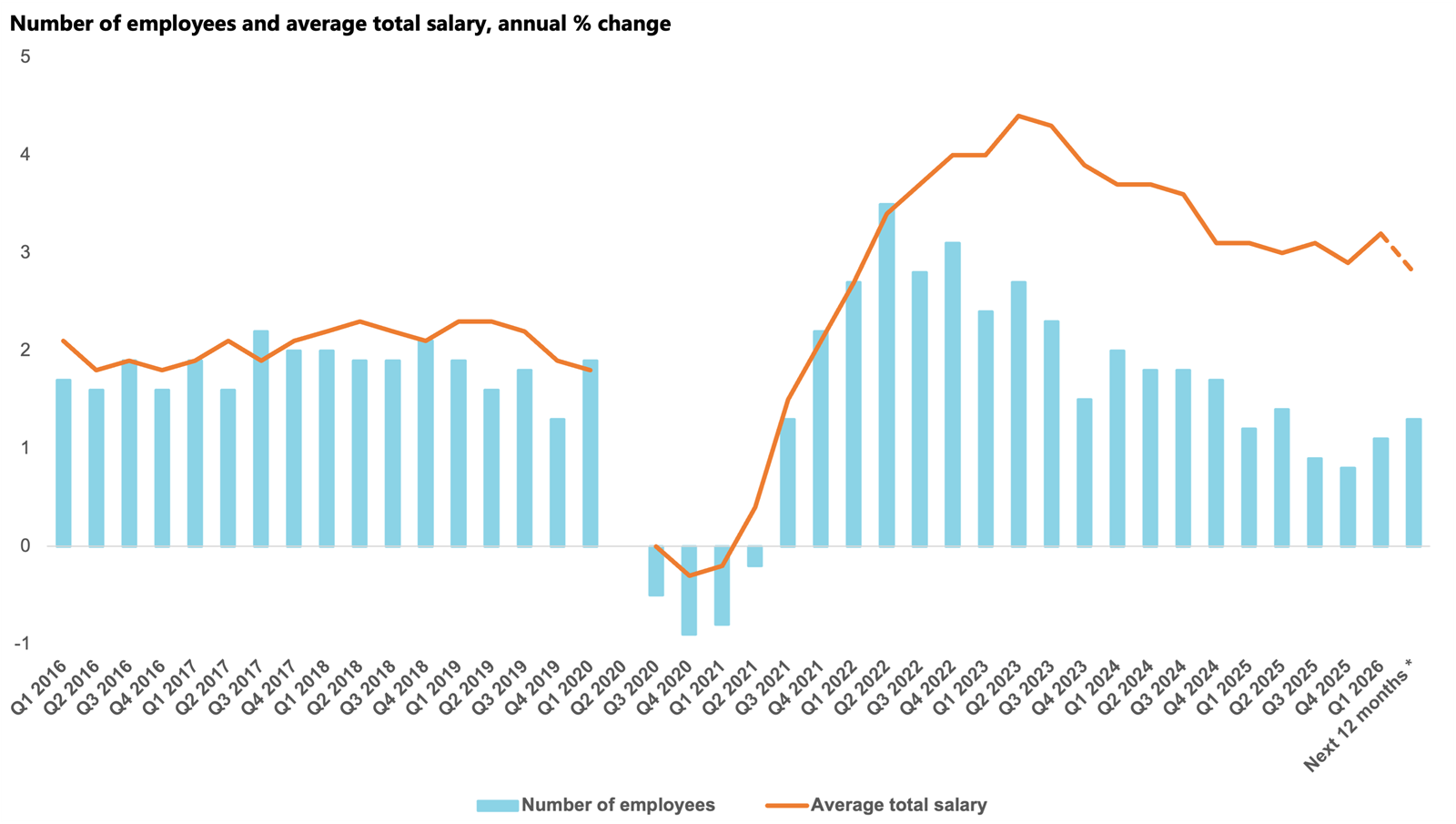

Employment growth picked up but remains modest as salary inflation gathers pace

- Employment growth picked up but remains below the historical norm and, while businesses plan to increase their staff levels at a slightly faster pace, numerous headwinds may limit gains over the coming year.

- IT & Communications companies anticipate the strongest employment growth of any sector, while companies in Construction and Property plan little workforce expansion.

- Annual salary inflation ticked up in Q1 2026, widening the gap with the historical average, though companies expect it to ease over the coming year.

Employment growth had been on a downward trend after the uplifts in employment costs related to last April’s rise in National Insurance Contributions and the National Living Wage (NLW) and concerns about the impacts of the Employee Rights Bill. However, there are tentative signs that labour demand was starting to return among UK businesses in Q1 2026, with companies reporting annual employment growth of 1.1%, up from 0.8% in the previous quarter, but still marginally lower than the historical norm (1.3%).

There remains wide variation between sectors, with employment in the Property sector declining by 0.7% year on year, the weakest outturn since Q1 2021, while the Construction sector recorded the largest uplift in headcount in the year to Q1 2026, growing by 2.6% y/y and more than double the national average.

A further modest uplift is anticipated over the next 12 months, with UK companies planning to raise their employment levels by 1.3%, equalling the national historical average. Businesses are likely to remain hesitant to expand headcount due to April’s 6.6% increase in the National Living Wage, pending changes included in the Employment Rights Bill, alongside the most recent rise in global uncertainty. At the sector level, Construction companies are particularly concerned about labour costs while Property businesses remain cautious following recent reductions in headcount. These sectors predict the most sluggish employment expansions, expecting growth of just 0.1% and 0.2%, respectively.

Meanwhile, the government’s plan to make the UK a “Global AI Superpower” ‒ by kick-starting AI adoption and building numerous data centres across the UK ‒ is seemingly fuelling growth expectations in the IT & Communications sector, with businesses anticipating employment growth of 2.9% over the next 12 months, the strongest of any sector.

Companies reported that annual wage inflation increased to 3.2% in the year to Q1 2026, widening the gap with the national historical average of 2.2%. Despite April’s increase in the NLW and potential additional costs associated with the Employment Rights Bill, companies expect salary growth to moderate slightly to 2.9% over the coming year. While most sectors predict salary growth will soften in the year ahead, IT & Communications is an exception, with a projected salary increase of 2.6%, compared with 2.3% in the previous 12 months. Business Services anticipates the next strongest uplift in salary growth at 3.1%, closely followed by Retail & Wholesale and Manufacturing & Engineering, which tend to employ larger proportions of workers in lower-paid roles, at 3.0%.

Weaker labour demand in recent quarters has meant concerns over labour availability have receded significantly. The proportions of businesses reporting both management and non-management skills availability as rising challenges dropped to five-year lows in Q1 2026, to 9% and 13%, respectively.

Profits and Investment

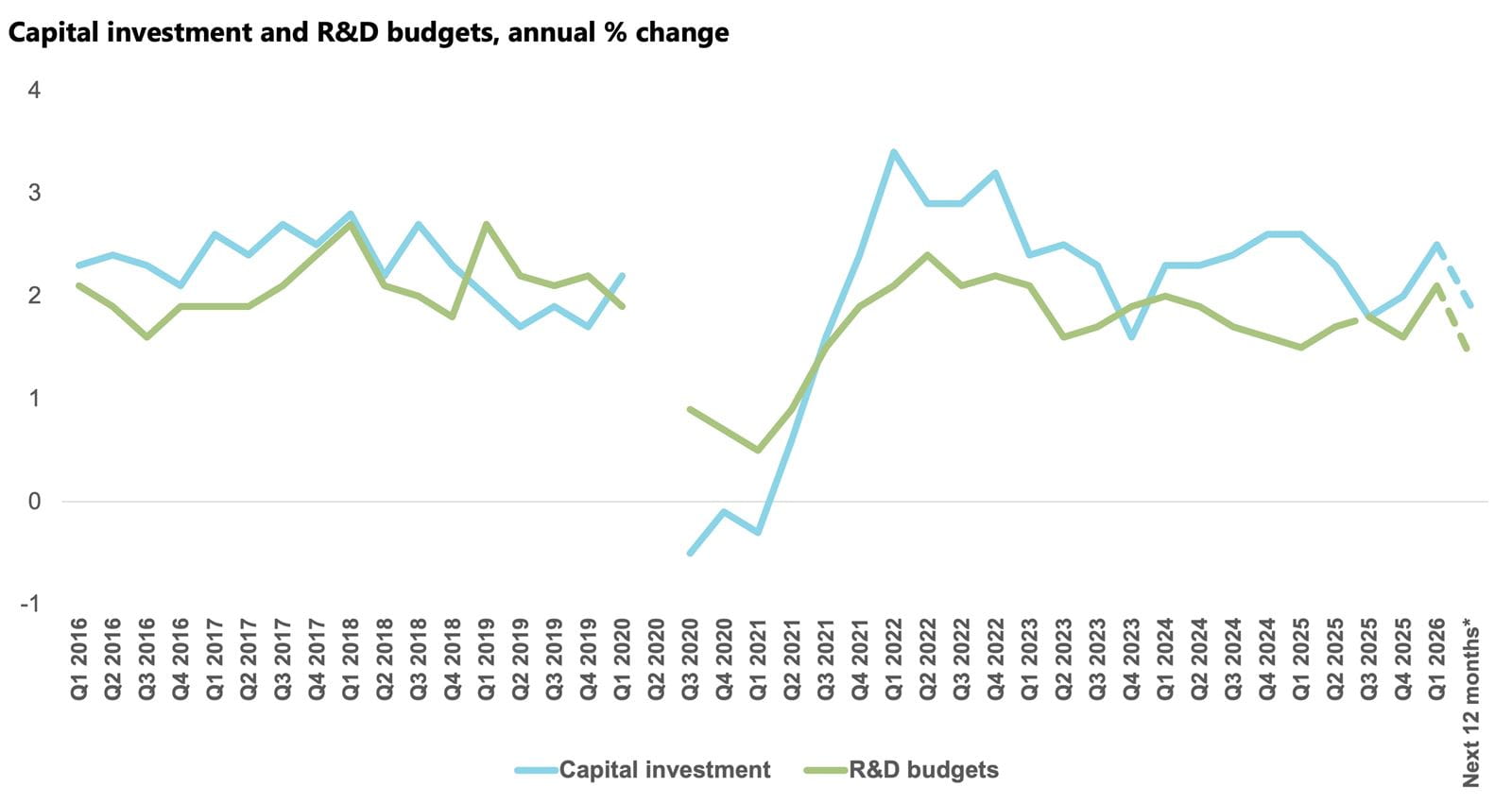

Iran war casts shadow over improved profits and investment growth

- Annual profits growth ticked up further in Q1 2026, climbing above the historical norm, but the Middle East conflict is likely to dampen otherwise upbeat expectations for the year ahead.

- Capital investment growth also increased, though businesses plan to moderate both capital investment and R&D budget growth over the next 12 months.

- Energy, Water & Mining companies reported the sharpest rise in capital investment growth but plan considerably slower expansion next year.

Improved domestic and export sales alongside easing inflation resulted in annual profits growth rising to 3.1% in Q1 2026, up from 2.7% in Q4 2025. The relatively strong outlook for domestic and export sales also fed into profit expectations of 5.2%. This forecast is significantly above the historical norm of 3.0% and is the highest projection since Q2 2024. However, most responses were collected before the US and Israeli intervention in Iran, and the subsequent spike in energy costs and uncertainty may cause businesses to moderate their outlook for the year ahead.

The improvement in profits growth and the Bank of England decision to gradually lower Bank Rate from 4.75% to 3.75% during 2025 supported a more favourable investment environment for businesses. Annual capital investment growth improved for the second consecutive quarter in Q1 2026, rising to 2.5%. However, borrowing costs are still high compared with pre-Covid levels and elevated uncertainty is weighing on investment decisions. As a result, companies plan to moderate growth in the year ahead to 1.9%, marginally below the historical norm of 2.0%.

Businesses have comparable expectations for their R&D budgets. Annual budget growth increased for the second consecutive quarter in Q1 2026, rising to 2.1%, above the historical average (1.8%), but companies plan to slow growth to just 1.4% over the next 12 months.

At the sector level, capital investment growth was strongest in Energy, Water & Mining, with a 4.7% uplift reported in Q1 2026. This comparatively strong rise was likely linked to the government’s continued transition towards net zero and the push to clean up UK waterways. However, this rapid rate of growth is expected to be short-lived, with businesses in the sector planning to slow capital investment growth over the coming year to just 2.6%, below the sector’s historical average of 3.0%. Indeed, most sectors plan to slow investment growth; only the Manufacturing & Engineering sector expects to increase it, projecting growth of 1.8% which is broadly comparable to the sector historical average (1.7%).

Confidence by sector

Sentiment improved in most sectors but varies widely, and is lowest in Retail & Wholesale, Transport & Storage and Construction

- Significant disparities in confidence remain between sectors, though sentiment improved overall in most sectors in Q1 2026. Transport & Storage was the only sector to record a decline.

- Confidence was strongest in Energy, Water & Mining, Banking, Finance & Insurance, and IT & Communications, while Retail & Wholesale, Transport & Storage and Construction were most pessimistic.

- Buoyant domestic sales growth underpins rising confidence in the most optimistic sectors, while labour costs and the tax burden weighed heavily on sentiment among Retail & Wholesale and Construction. Energy costs are of greatest concern in Transport & Storage.

Stronger domestic and export sales outlooks meant business confidence improved across most sectors overall in Q1 2026, though the Iran conflict is likely to dampen much of this optimism. Confidence was strongest among Energy, Water & Mining companies, which moved into positive territory in Q1 2026, reaching +12.9 ‒ nearly double the sector’s historical average (+6.6). The uptick was likely linked to strong domestic sales growth in the year to Q1 2026, which, at 5.0%, outpaced all other sectors, and to concerns about the tax burden dissipating after the government announced it was ending funding for the Energy Company Obligation scheme and moving 75% of the costs of the Renewables Obligation to general taxation.

More broadly services sectors in Banking, Finance & Insurance (+4.7), IT & Communications (+2.5) and Business Services (+2.3) are more positive than the UK average but their scores remain below their respective historical survey norms. Sentiment in Manufacturing & Engineering (+1.7) moved into positive territory amid improved annual domestic and export sales growth but weekly survey data shows that confidence in the sector was shaken by events in the Middle East.

In contrast, Retail & Wholesale businesses were the most pessimistic, with the Business Confidence Index at -11.0. The labour-intensive nature of the sector means it was particularly exposed to the increases in employers’ National Insurance Contributions last April and to the increase in the National Living Wage set for April 2026. Over two thirds (69%) of Retailers cited labour costs as a growing issue over the past 12 months ‒ more prevalent than in any other sector ‒ while citations of the tax burden were still over three-times higher than the sector’s historical average (19%), at 61% of businesses surveyed.

Transport & Storage was the only sector to report a decline in confidence between Q4 2025 and Q1 2026, dropping from -0.8 to -9.7. This decline is likely to be partly attributable to heightened global uncertainty following the escalation of the conflict in the Middle East and rising fuel prices, as well as comparatively weak domestic sales (2.8%) and export sales (1.9%), lagging both their respective historical and national averages.

All sectors reported a slowdown in annual input cost inflation in Q1 2026 compared with the previous quarter, and all expect that inflation will remain flat or moderate further over the coming year, though most expectations were set before the onset of the Iran war. Nevertheless, plans to raise selling prices vary by sector. Companies in the Transport & Storage and Energy, Water & Mining sectors plan to increase their selling prices at the sharpest pace, at 2.9% and 2.8%, respectively ‒ second only to Business Services, which expects growth of 3.0%. Businesses in the Banking, Finance & Insurance sector anticipate the softest rise, with a projected increase of just 0.8% over the coming year.

Confidence by region and nation

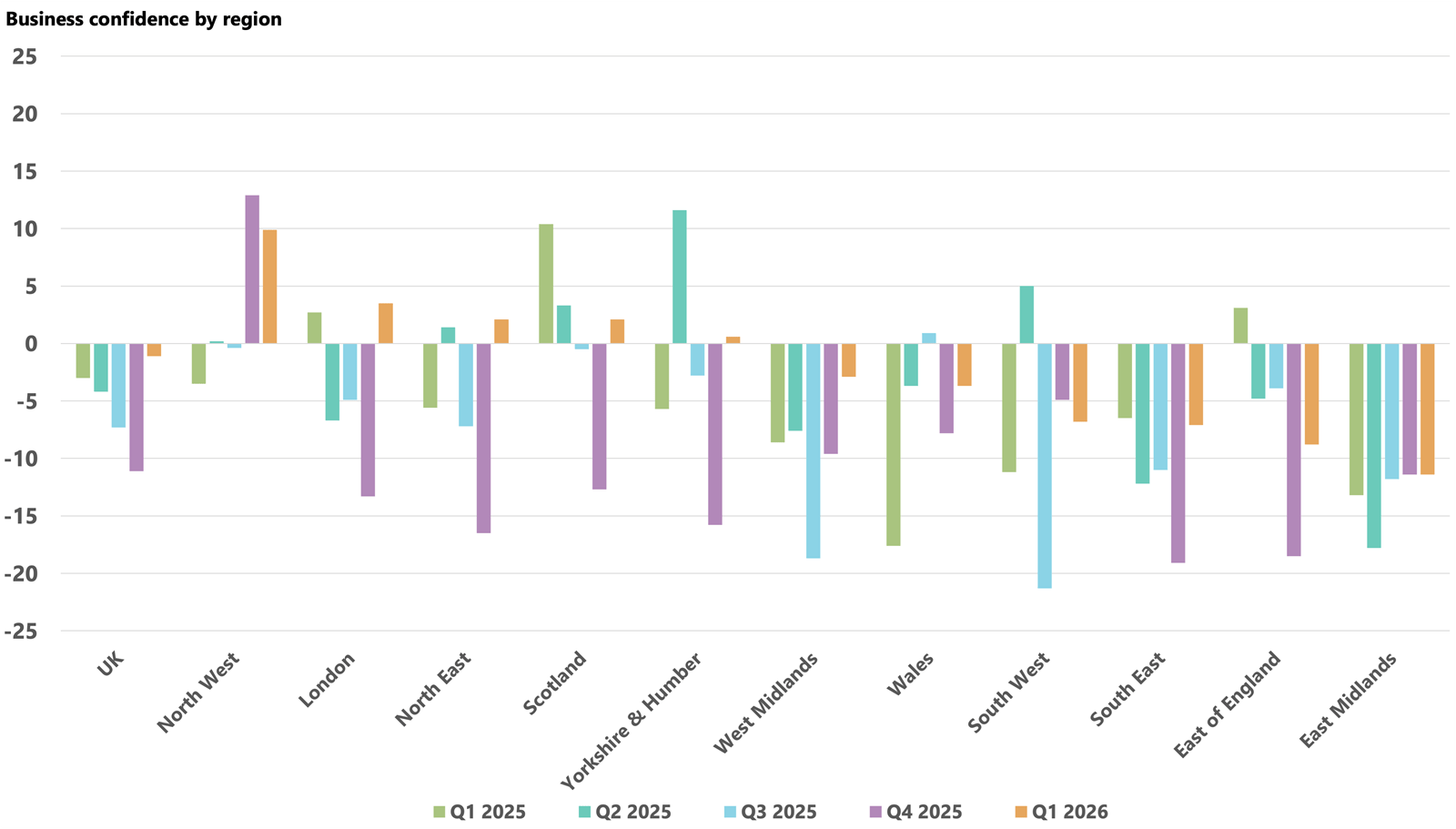

Confidence rose in most regions, with London, Scotland, the North East and Yorkshire & Humber joining the North West in positive territory

- Confidence improved across most UK regions in Q1 2026, with four regions moving out of negative territory.

- The North West and London were the most optimistic. Companies in the East Midlands were the most pessimistic in the UK, with confidence unchanged from the previous quarter.

Sentiment improved in most UK regions in Q1 2026 as concerns about the tax and regulatory burden eased, with only the North West and South West reporting a decline in confidence compared to the previous quarter. Despite this modest drop, businesses in the North West remained the most optimistic of all UK regions in Q1 2026, with the Business Confidence Index easing from +12.9 to +9.9.

Companies in the East Midlands are now the most pessimistic in the UK, with confidence unchanged in Q1 2026 compared to the previous quarter at -11.4. The turbulent global trading environment has likely contributed to the region’s lack of optimism, given the region’s greater dependence on production and logistics, which means businesses are more exposed to spikes in energy prices as well as to weaker global demand.

Further analysis of confidence for each region and nation is available in their respective reports on ICAEW Business Confidence Monitor.

Confidence by business size

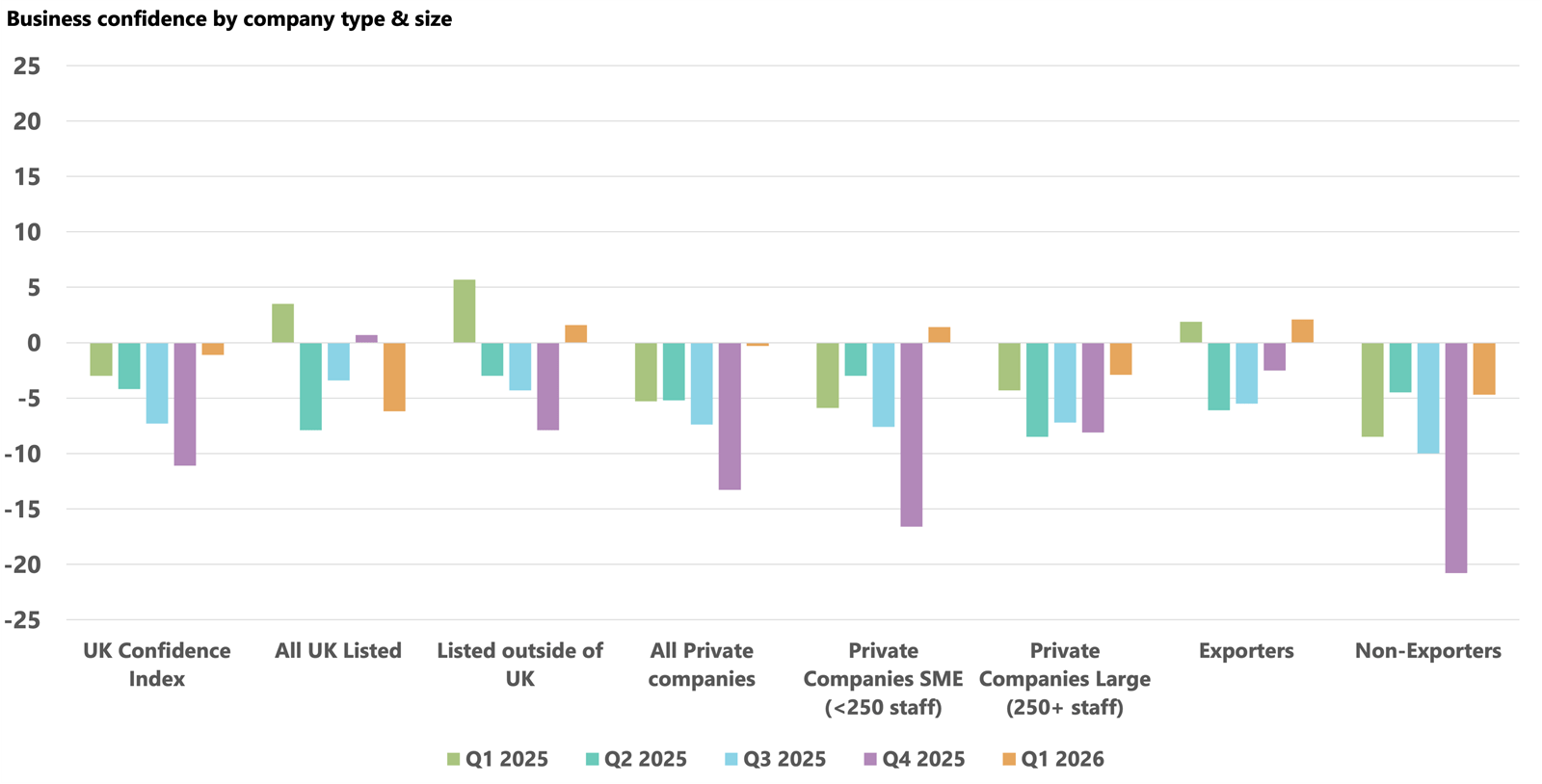

The sentiment gap between smaller and larger companies has narrowed, while exporters are most optimistic about prospects

- Sentiment improved across most company types and sizes, with exporters the most optimistic.

Business sentiment improved for most company types and sizes in Q1 2026. Survey results indicate that exporters were the most confident, with their Business Confidence Index rising from -2.5 in Q4 2025 to +2.1. The gap in confidence between small private companies with fewer than 250 staff and large private companies narrowed significantly compared to the previous quarter.

Economic and political environment during the survey period

Inflation risks rise amid Middle East conflict as underlying UK economic growth remains weak

- The outbreak of the Iran war in late February caused a spike in oil and gas prices and a rise in global uncertainty, impacting the economic outlook for the UK.

- Evidence of rising inflation caused the Bank of England to hold interest rates in March.

- UK economic growth was muted before the conflict with GDP flat in January, but there were tentative signs of improvement as inflation continued to ease and retail sales picked up.

Economic conditions declined sharply towards the end of the survey period following the escalation of conflict in the Middle East at the end of February. Oil and gas prices spiked with the burden starting to feed through to consumers, with high frequency data showing petrol prices rising significantly since the war began. Evidence of inflationary pressures impacted the Bank of England’s decision to hold Bank Rate at 3.75% in their March meeting – a cut had been widely expected before the outbreak of war.

The rise in energy prices is set to filter through more widely and start to drive up general inflation, reversing some of the progress that had been made earlier in the survey period when inflation continued to cool, with annual CPI inflation dropping to 3.0% in the year to February, down from 3.4% in December. Pay pressures also eased as private sector regular pay growth dropped back to 3.3% in January from 4.2% in the three months to October. The OFGEM energy price cap will fall by 6.7% in April, protecting households from price rises in the near term, but domestic energy prices are likely to rise significantly from July when the next change in the price cap comes into force.

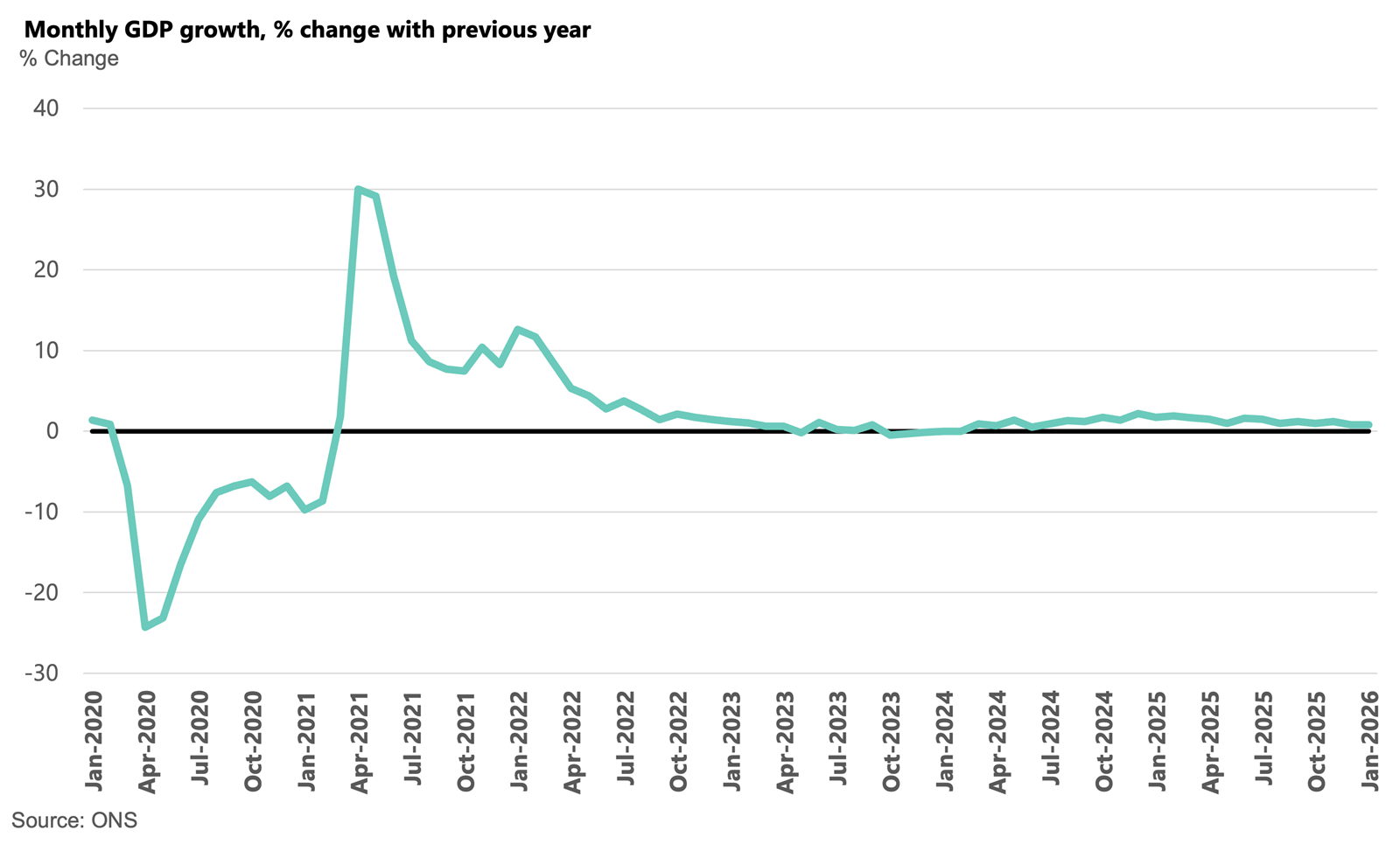

The Iran war came at a time when some economic indicators were showing signs of improvement. Alongside easing inflation, monthly retail sales volumes rebounded sharply by 1.8% in January 2026, before easing back by 0.4% in February. There were also tentative signs that labour market conditions started to improve as provisional payroll employment figures ticked up in January and February. Despite these tentative signs of recovery, the UK economy entered 2026 carrying little momentum as monthly GDP data showed the economy failed to expand in January 2026 and was flat at 0.0% compared to December 2025, following growth of just 0.1% in both Q3 and Q4 2025. While prospects may have looked a little better in February, the unfolding events in the Middle East have likely weakened UK economic growth prospects for March and the year ahead.

How to grow

Support from ICAEW on starting, growing and renewing businesses in the UK, and supporting the government's mission of kickstarting sustainable economic growth.