Q4 2025: Retail & Wholesale suffers further slump in confidence as challenges mount.

The latest national Business Confidence Monitor (BCM) shows that business sentiment slipped deeper into negative territory amid uncertainty about the Budget and rising concern about both the tax burden and regulations. However, companies are optimistic that domestic sales and exports growth will improve over the next 12 months.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 8 October to 11 December 2025.

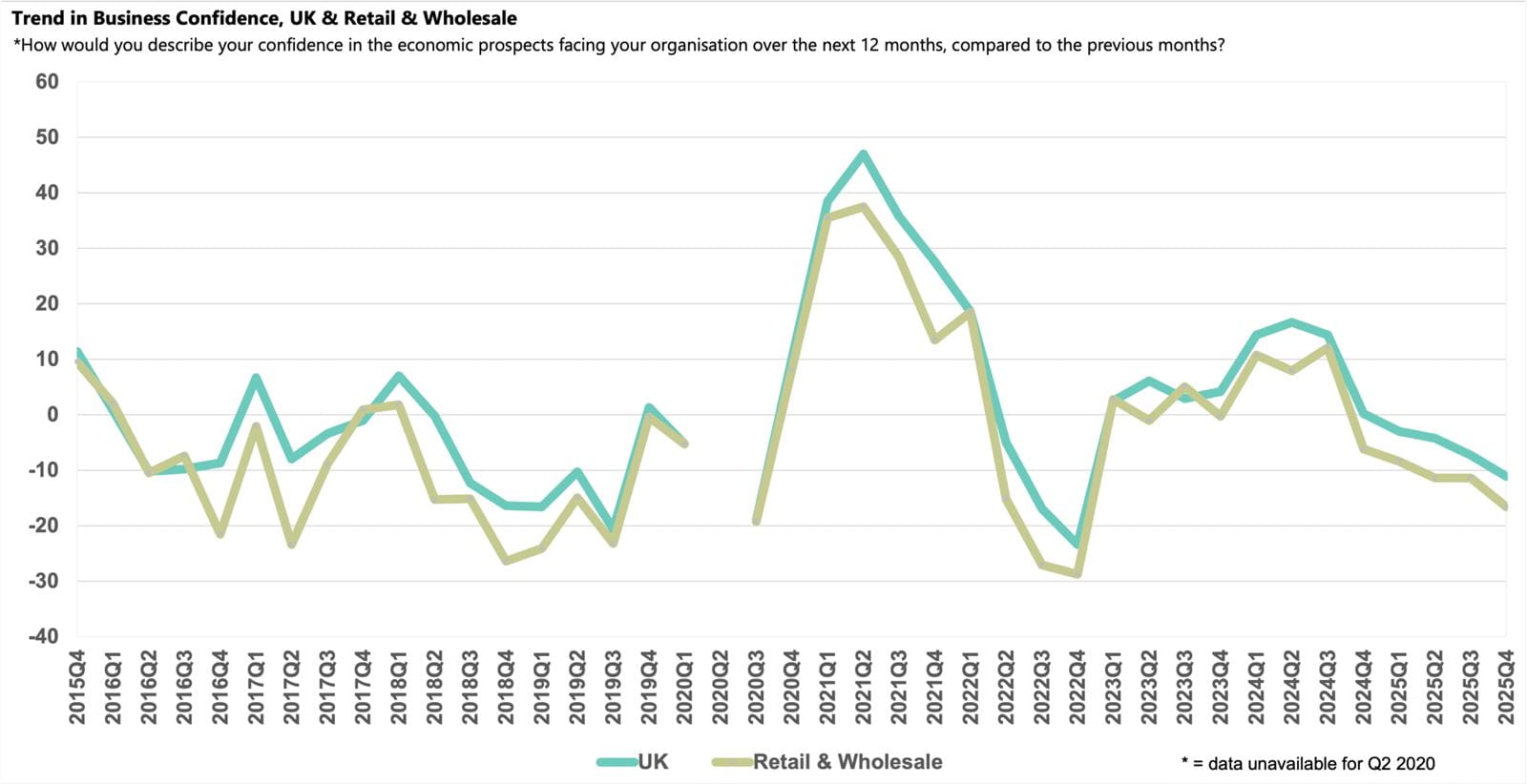

- The Business Confidence Index for Retail & Wholesale slipped into deep negative territory to -16.6 in Q4 2025, significantly below both the UK (-11.1) and historical (-0.4) averages.

- Domestic sales growth edged up but, with consumer confidence remaining fragile, companies are increasingly concerned about customer demand.

- The tax burden remained the most prevalent rising challenge, while concern about regulatory requirements reached a record high and competition in the marketplace rose to a near eight-year high.

- Employment continued to decline in the year to Q4 2025 but businesses plan modest jobs growth next year.

- Annual input price inflation rose to the highest rate since Q1 2024 and the rise in selling prices in Retail & Wholesale was among the strongest of all sectors.

- Prospects for both capital investment and R&D budgets are relatively subdued.

Business confidence in the Retail & Wholesale sector

Confidence in Retail & Wholesale dropped further to reach -16.6 in Q4 2025 from -11.4 in Q3 2025, remaining below the UK average (-11.1) and significantly lower than the historical sector average (-0.4). Sentiment among Retail & Wholesale businesses was weaker than all other UK sectors apart from Property companies (-23.4).

The fall in confidence reflects the range of challenges facing the Retail & Wholesale sector, with several growing issues at survey highs this quarter. Consumer confidence remains subdued and businesses’ concern about customer demand rose sharply in Q4 2025, matching the survey record high outside of the pandemic period. The December 2025 Bank of England Agents’ Summary of Business Conditions stated that consumers are generally less inclined to make discretionary purchases, with the November Budget regularly cited by contacts as discouraging spending in recent months. The BCM found that concern about the tax burden remained at historically high survey levels in Retail & Wholesale in Q4 2025. Meanwhile, the 2025 Employment Rights Bill received Royal Assent in late 2025 and is set to provide a considerable shake-up to operating practices in the sector and likely contributed to the increase in regulatory concerns reported in the sector, reaching another survey record high this quarter.

Domestic sales growth and customer demand

Amid challenging conditions for Retailers & Wholesalers, annual domestic sales growth edged up in Q4 2025 to 3.0%, broadly matching the sector’s historical norm and national average (both 2.9%). Businesses remain optimistic about sales prospects and expect growth to rise to 3.6% over the coming year, although this is weaker than the average projected across all sectors (4.2%). The relatively subdued outlook is underpinned by growing concern about customer demand in the sector, which was reported by 61% of businesses in Q4 2025, matching the high seen in Q4 2008 during the Global Financial Crisis and only just below the record survey high logged in Q3 2020 (64%) during the pandemic. The issue was more prominent than in any other sector and notably above the sector norm (44%) and the national average (41%).

Business challenges

While concern about customer demand rose sharply, the tax burden remains the most prevalent growing challenge for the Retail & Wholesale sector, reported by 66% of businesses and matching the survey historical high recorded last quarter. Sustained concern at nearly four times the survey norm (18%) reflects a combination of April’s tax rises and pre-Budget uncertainty.

After customer demand (61%), regulatory requirements were the next most widespread rising concern for companies in the Retail & Wholesale sector, with reports increasing to 55% of businesses in the sector, a new survey record, and significantly above historical norm of 35%. This uplift in concern is undoubtedly linked to the Employment Rights Act, which passed into law in late 2025. With consumers continuing to shop around to find the best deals, concern about competition in the marketplace also rose and was cited by 51% of businesses, the highest proportion since Q1 2018 and above the historical average (40%).

Labour market

Employers in the sector reported another decline in jobs in the year to Q4 2025, with employment falling by 0.1% and the third consecutive quarter of job losses. However, the pace of contraction slowed sharply from the previous quarter and businesses plan to grow their workforces next year, with employment expected to expand by 0.3% over the coming 12 months. However, concerns about the impact of the Employment Rights Act are no doubt weighing on the outlook, as the projection is weaker than the sector historical norm (0.8%) and significantly weaker than the national growth projection of 1.3%.

During a downturn in labour demand in the sector, concerns about skills availability and staff turnover have eased greatly and in Q4 2025 were below both the national average and their respective historical norms. As well as affecting employment demand, rising employment costs following April’s tax rises have also had a negative impact on training budgets in Retail & Wholesale, with businesses reporting no growth in annual budgets from the previous quarter. This was the lowest reading since the pandemic period and significantly below the average growth in the sector (1.0%). Companies plan to grow their training budgets by 1.1% next year, broadly in line with the national average (1.2%).

Annual wage inflation also slowed to 2.6% in Q4 2025, down from the previous quarter and now closer to the sector historical average (2.0%). However, companies expect the pace of pay growth to increase slightly to 2.7% over the coming 12 months, a view which is broadly consistent with the UK average forecast (2.8%).

Input and selling prices, and profits growth

Businesses reported a further rise in input price inflation in Q4 2025, to 4.1%, the highest rate in the Retail & Wholesale sector since Q2 2024 and matching the national average. Companies anticipate input price growth to slow to 3.0% in the year ahead, also equalling the UK projection.

The growth in selling prices in the sector also ticked up, rising to 2.9% in Q4 2025, among the strongest price rises recorded across UK sectors and second only to Transport & Storage (3.1%). Businesses in the sector plan to raise their prices by 2.5%, slightly higher than the UK forecast (2.2%) and notably ahead of the historical sector norm (1.6%).

Despite the challenging market conditions, companies reported an uptick in annual profits growth to 3.1% in Q4 2025, outperforming the sector historical (2.3%) and national (2.7%) averages. Retail & Wholesale businesses are optimistic that profits growth will rise to 3.9% in the year ahead, only a little weaker than the UK outlook (4.3%).

Investment

Capital investment growth rose to 1.6% in Q4 2025, close to the norm for the Retail & Wholesale sector (1.7%). However, this was weaker than the national average of 2.0% and, with businesses planning to slow growth to just 1.0% next year compared to 1.6% on average across the UK, companies in the sector are relatively downbeat about investment prospects.

Businesses are similarly pessimistic about R&D budget growth, which dipped to 0.7% in the year to Q4 2025, less than half the national average (1.6%). Companies intend to maintain growth at a similar rate of 0.8% next year, notably lower than the sector norm (1.4%).