ICAEW sets out its vision for local audit, making the case for better financial reporting, high quality and more timely audits, stronger financial management and governance, and a thriving profession that is highly valued.

The local financial reporting and audit system in England is in crisis. The proportion of local authorities in England that have published their audited financial statements on time has fallen from more than 95% in 2017 to less than 12% in 2022. This has knock-on effects for the audits of other local public bodies such as in the NHS.

High-profile governance failures have led to significant financial losses. Impenetrable financial statements are not well understood and are not being used effectively to hold local public bodies to account. There is insufficient capacity in the local audit market, while auditors, finance teams and regulators are not aligned in their view of audit risks. Under-resourced finance teams struggle to produce good quality working papers. Local authority finance teams and audit firms struggle to retain staff in the profession.

In response to this crisis, ICAEW has put together a vision for local audit that sets out our support for understandable financial reports, timely high-quality local audits, strong financial management and good governance, value for money and protecting the public interest, and the critical role accountants and auditors play in enhancing transparency and accountability in the public sector.

We are publishing our vision for local audit following the publication of the Memorandum of Understanding (MoU) between the Department of Levelling Up, Housing and Communities (DLUHC) and the Financial Reporting Council (FRC) on 2 March 2023. We welcome the MoU, which covers the role of the shadow system leader for local audit pending the establishment of the Audit, Reporting and Governance Authority (ARGA).

We also believe more needs to be done urgently if the local financial reporting and audit crisis is to be resolved.

ICAEW's vision for local audit is designed to prompt discussion, identifying a series of challenges we believe need to be overcome, and actions we support to address those challenges.

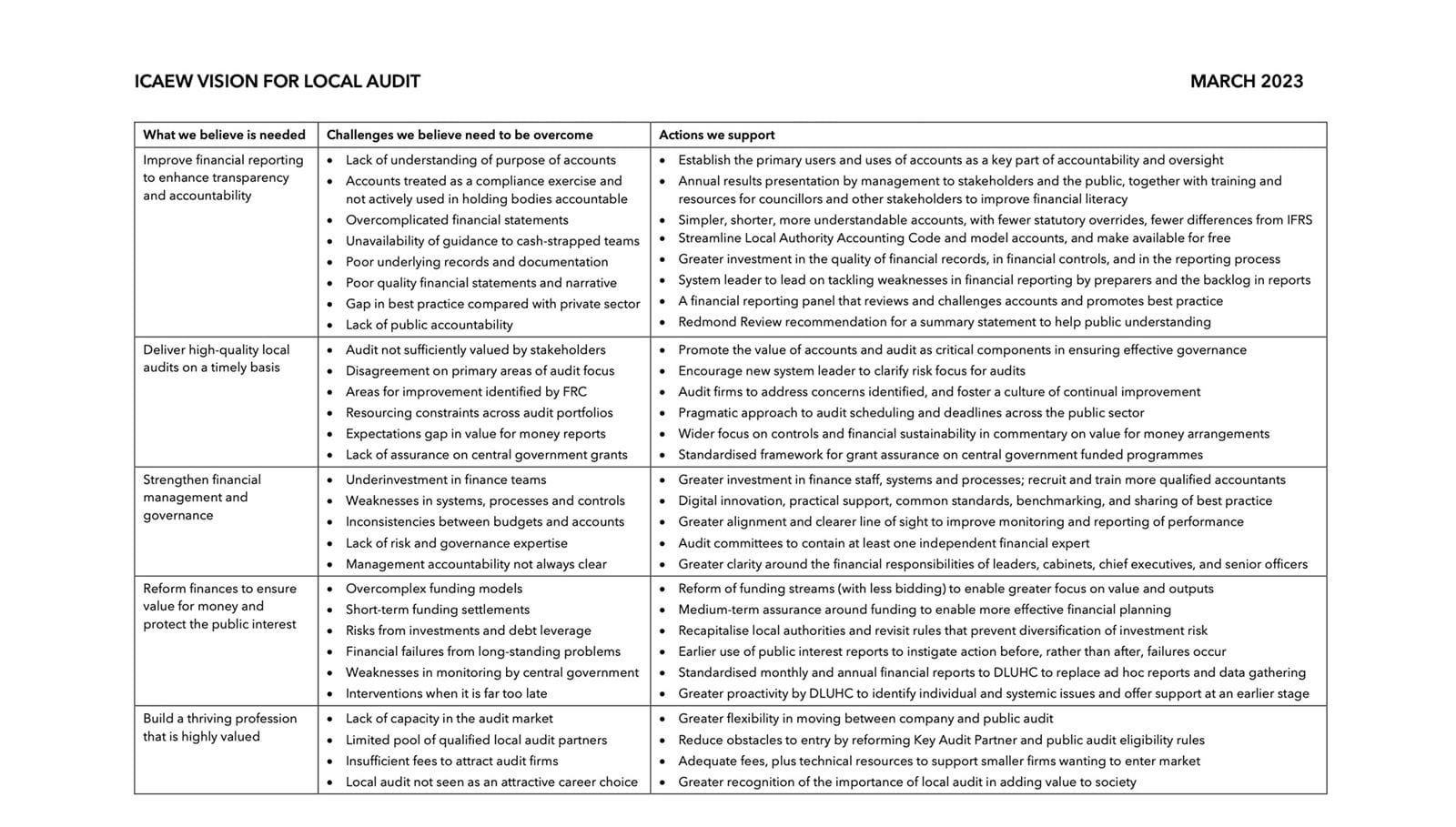

Improve financial reporting to enhance accountability

Our vision starts with the principle that producing high-quality transparent financial reports is essential to effective decision-making, good governance and accountability, as well as being a key element in the system of financial control.

We support re-examining financial reporting by local public bodies to ensure the annual report and accounts are fit for purpose and are core to the process of holding local public bodies to account. We would also like to see streamlining and simplification of annual reports and financial statements to make them understandable and more usable, as well as ensuring local finance teams are properly equipped to produce hiqh-quality financial reports that meet the needs of all stakeholders.

| Challenges we believe need to be overcome | Actions we support |

|---|---|

| Lack of understanding of the purpose of accounts | Establish the primary users and uses of accounts as a key part of accountability and oversight |

| Accounts treated as a compliance exercise and not actively used in holding bodies accountable | Annual results presentation by management to stakeholders and the public, together with training and resources for councillors and other stakeholders to improve financial literacy |

| Overcomplicated financial statements | Simpler, shorter, more understandable accounts, with fewer statutory overrides, fewer differences from IFRS |

| Unavailability of guidance to cash-strapped teams | Streamline Local Authority Accounting Code and model accounts, and make available for free |

| Poor underlying records and documentation | Greater investment in the quality of financial records, in financial controls, and in the reporting process |

| Poor quality financial statements and narrative | System leader to lead on tackling weaknesses in financial reporting by preparers and the backlog in reports |

| Gap in best practice compared with private sector | A financial reporting panel that reviews and challenges accounts and promotes best practice |

| Lack of public accountability | Redmond Review recommendation for a summary statement to help public understanding |

Deliver high-quality, timely local audits

We believe that high-quality financial statements need to be accompanied by high-quality external audits to provide the assurance stakeholders need, when they need it. Delays in publishing audited financial statements need to be tackled urgently if confidence in local finances is to be restored.

Resource is a major issue for audit teams, and a pragmatic approach is needed in how audits are scheduled across local authority, local NHS bodies, academy schools and other local public bodies.

| Challenges we believe need to be overcome | Actions we support |

|---|---|

| Audit not sufficiently valued by stakeholders | Promote the value of accounts and audit as critical components in ensuring effective governance |

| Disagreement on primary areas of audit focus | Encourage new system leader to clarify risk focus for audits |

| Areas for improvement identified by the FRC | Audit firms to address concerns identified, and foster a culture of continual improvement |

| Resourcing constraints across audit portfolios | Pragmatic approach to audit scheduling and deadlines across the public sector |

| Expectations gap in value for money reports | Wider focus on controls and financial sustainability in commentary on value for money arrangements |

| Lack of assurance on central government grants | Standardised framework for grant assurance on central government funded programmes |

Strengthen financial management and governance

We believe that weaknesses in how audited financial statements are being used, combined with delays in their publication, are symptomatic of underlying issues in financial management and governance in some English local authorities.

All local authorities need audit committees that contain at least one independent member with financial, risk and governance expertise to complement councillors in exercising oversight over council leadership and management teams.

| Challenges we believe need to be overcome | Actions we support |

|---|---|

| Underinvestment in finance teams | Greater investment in finance staff, systems and processes; recruit and train more qualified accountants |

| Weaknesses in systems, processes and controls |

Digital innovation, practical support, common standards, benchmarking, and sharing of best practice |

| Inconsistencies between budgets and accounts |

Greater alignment and clearer line of sight to improve monitoring and reporting of performance |

| Lack of risk and governance expertise | Audit committees to contain at least one independent financial expert |

| Management accountability not always clear | Greater clarity around the financial responsibilities of leaders, cabinets, chief executives, and senior officers |

Reform finances to ensure value for money and protect public interest

Reform is needed in how local authorities are financed, enabling them to concentrate on ensuring value for money in how they deliver local public services and in how they manage financial exposures. More proactivity is needed to identify potential failures in local authority governance and for interventions at an earlier stage than has been the case.

Local authorities need to do more to protect the public interest, but so does central government.

| Challenges we believe need to be overcome | Actions we support |

|---|---|

| Overcomplex funding models | Reform of funding streams (with less bidding) to enable greater focus on value and outputs |

| Short-term funding settlements | Medium-term assurance around funding to enable more effective financial planning |

| Risks from investments and debt leverage | Recapitalise local authorities and revisit rules that prevent diversification of investment risk |

| Financial failures from long-standing problems |

Earlier use of public interest reports to instigate action before, rather than after, failures occur |

| Weaknesses in monitoring by central government | Standardised monthly and annual financial reports to DLUHC to replace ad hoc reports and data gathering |

| Interventions when it is far too late |

Greater proactivity by DLUHC to identify individual and systemic issues and offer support at an earlier stage |

Build a thriving profession that is highly valued

Underpinning our vision is the need for a thriving profession that attracts talented individuals to work in the sector. ICAEW welcomes the recent five-year procurement round that saw the number of audit firms participating rise and an increase in fees that will contribute to local audit being more viable.

We continue to argue for fewer obstacles to entry to the market, as well as ensuring that those working in local audit feel valued for the contribution they make in enabling public services to be delivered, communities and local economies to develop, and in protecting public money and resources.

| Challenges we believe need to be overcome | Actions we support |

|---|---|

| Lack of capacity in the audit market |

Greater flexibility in moving between company and public audit |

| Limited pool of qualified local audit partners | Reduce obstacles to entry by reforming Key Audit Partner and public audit eligibility rules |

| Insufficient fees to attract audit firms |

Adequate fees, plus technical resources to support smaller firms wanting to enter the market |

| Local audit not seen as an attractive career choice | Greater recognition of the importance of local audit in adding value to society |

Implementing our vision for local audit

This vision has provided ICAEW with a focus for our engagement with local authorities, auditors, government and regulators, provoking debate and, we hope, encouraging everyone involved to take action. Our vision extends to the whole of the local audit sector covering local government, NHS bodies, fire and rescue authorities, local police bodies, internal drainage boards and national park authorities, but our focus is on local authorities where there is the most need for change.

We have been pleased with the level of engagement we have received in discussing our vision for local audit. ICAEW and CIPFA are looking into how narrative reports and financial statements can be made more understandable and usable to encourage greater use.

The Levelling Up, Housing and Communities Committee has launched an inquiry into the purpose, understanding and impact of financial reporting and audit in local authorities.

The MoU between DLUHC and the FRC provides a foundation for addressing many of the challenges in the system, and DLUHC is moving forward with many of the recommendations of the Redmond Review and from its December 2021 proposals.

However, much more still needs to be done and we hope to continue to use our vision as an evolving agenda for change.

Resources

Public sector

See the latest insights and support on public sector finance, audit, financial management and financial reporting.

ICAEW Community

Public Sector Community

The go-to place for guidance on issues affecting finance professionals working in and with the public sector. With a range of dynamic services, ICAEW provides valuable tools, resources and support tailored to the public sector.

Insights special

Public sector financial and non-financial reporting

This special highlights the vital role public sector reporting plays in strengthening financial controls, improving evidence-based decision making and bringing transparency to the public about how taxpayers’ money is spent.

Find out more