Q4: Sentiment rises but record concerns about the tax burden leave the score in negative territory.

The latest national Business Confidence Monitor (BCM) shows that business sentiment slipped deeper into negative territory amid uncertainty about the Budget and rising concern about both the tax burden and regulations. However, companies are optimistic that domestic sales and exports growth will improve over the next 12 months.

The survey results are based on 1,000 telephone interviews among ICAEW Chartered Accountants covering a range of UK sectors, regions and company sizes, ensuring a representative picture of the UK economy. The latest quarterly findings are based on the period 8 October to 11 December 2025.

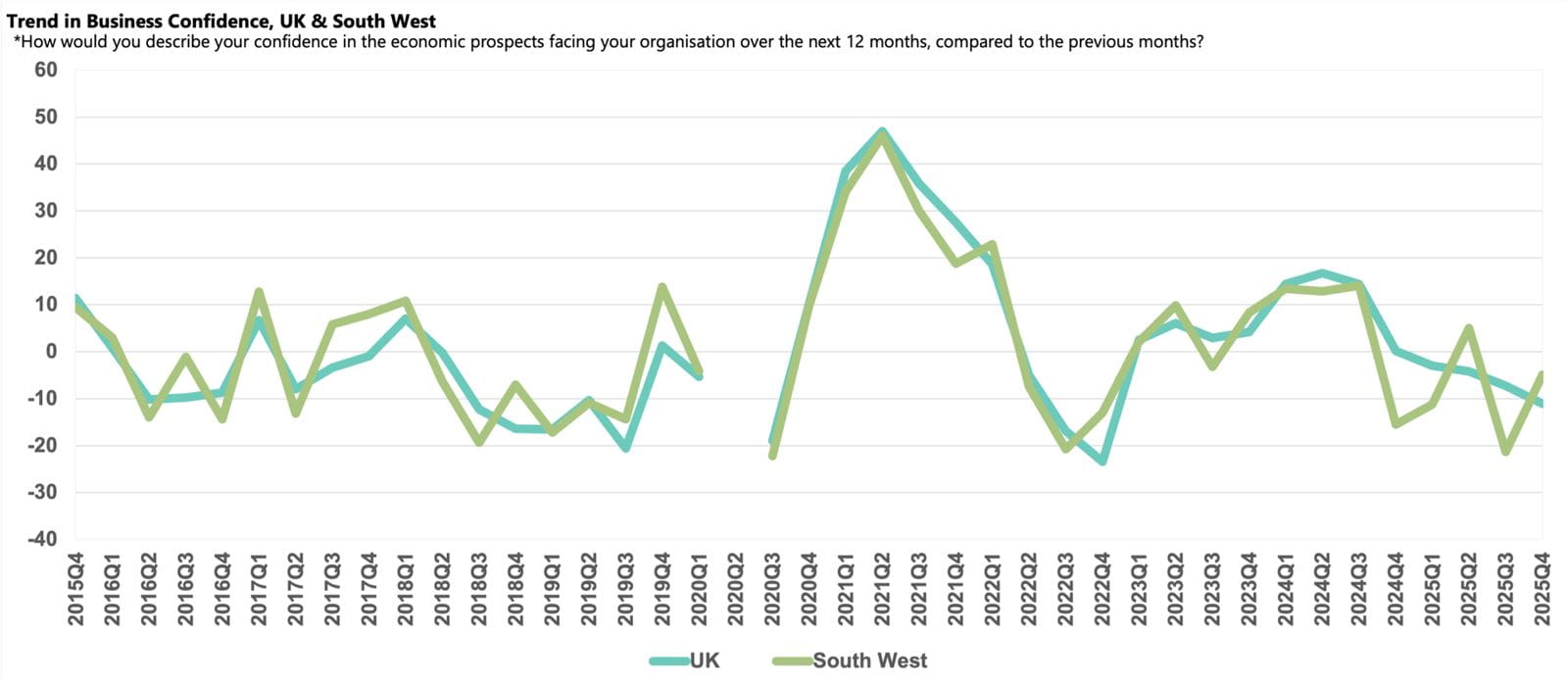

- Confidence among businesses in the South West rose to -4.9, ahead of the UK score (-11.1) but still below the regional norm (+3.5).

- Relatively strong domestic and export sales growth buoyed sentiment in the region but businesses reported record high concerns about the tax burden.

- Regulatory issues also rose to the highest rate since Q2 2018 and input price inflation and salary inflation both edged up, dampening profits growth.

- However, businesses expect strong domestic sales to drive profits growth next year and hold the most optimistic outlook of any region.

- After cooling last quarter, employment growth returned to above average rates, with similar growth expected next year.

- Capital investment growth edged ahead of the historical average and businesses intend to maintain that rate of growth alongside a significant boost to flagging R&D growth.

Business confidence in South West

The confidence score in the South West improved in Q4 2025, rising to -4.9 from -21.3 last quarter. Despite sentiment remaining below the historical average (+3.5), companies in the region are now among the most confident in the UK, behind only the North West, which was the only region to record a positive score. In contrast, average UK business confidence dropped further to -11.1.

The pick-up in confidence likely reflects the region’s relatively buoyant domestic sales and exports growth, with both running ahead of their respective historical norms and above the UK average. However, businesses in the South West are the most concerned about the tax burden in the UK, fuelled by pre-Budget anxiety after April’s tax rises. Changes to inheritance tax impacting farms announced in the Autumn 2024 Budget is believed to have negatively impacted sentiment in the region. However, in late December 2025, the government performed a partial U-turn and raised the inheritance tax relief threshold to £2.5m for farmers from next April.

Domestic sales and exports growth

Domestic sales continued to expand at an above average rate in Q4 2025, with annual growth of 3.2%, remaining above the historical norm (3.1%) and the UK average (2.9%). Companies are also more optimistic than they were last quarter and now predict growth of 5.5% in the year ahead, compared to the national projection of 4.2%. The outlook of businesses in the locally important Energy, Water & Mining and Business Services sectors are likely supporting this view.

More positive still was the reported uptick in exports growth in Q4 2025, rising to 2.9%, the highest rate since Q1 2025 and above the regional historical average (2.7%). The uplift in exports growth is expected to continue next year, with businesses projecting growth of 3.3%. However, this is somewhat weaker than the national forecast (4.1%) and it is likely that the more pessimistic views of Energy, Water & Mining and Manufacturing & Engineering companies in the region are weighing on the outlook.

Input price, selling prices and profits growth

Input price inflation continues to be sticky for South West businesses as they reported growth of 4.3% in the year to Q4 2025, edging up slightly from the previous quarter and further from the regional historical norm (2.9%). Companies anticipate input cost growth will ease to 3.0% over the coming 12 months, matching the national projection.

Businesses also raised their prices at a faster rate in Q4 2025, increasing selling prices by 2.7% in the year, ahead of the national average (2.3%). Reflecting the stickiness of their costs, companies in the South West expect their selling price growth to edge up to 2.8% over the coming 12 months, the fastest rate projected across regions and above the UK average (2.2%).

Cost pressures appear to be a drag on profits growth in the region and, despite buoyant sales growth, profits expanded by just 2.0% in the year to Q4 2025. This was both weaker than the historical norm (3.0%) and the national average (2.7%). However, businesses expect growth to accelerate rapidly in the coming year to 5.9%, the fastest rate predicted in the UK.

Labour market

Having slowed significantly in Q3 2025, businesses in the South West reported that annual employment growth rose to 2.3% in Q4 2025, second only to the West Midlands (2.9%) and above the national average of just 0.8%. Companies are also relatively upbeat about their recruitment plans for the year ahead, planning to increase employment by 2.0%, which remains above the historical norm (1.5%) and the national projection (1.3%).

Alongside rising input cost pressures, salary inflation also ticked up for businesses in the South West. They reported that wages rose by 3.3% in the year to Q4 2025, above the UK average (2.9%). Companies anticipate that the upward pressure on pay will ease to 2.8% in the coming 12 months, consistent with the national expectation but notably above the regional historical norm (2.2%).

Ongoing skills supply issues in the South West may help explain the above average pay growth, with the availability of management and non-management skills being a more prominent issue among businesses in the region than nationally.

Business challenges

Businesses in the South West were most likely to report the tax burden as a growing challenge in Q4 2025, cited by 71% of companies, the highest proportion of any region. This marked another survey high at nearly four times the regional norm (18%), amid pre-Budget uncertainty and following April’s tax rises. Regulatory concerns rose to their highest rate since Q2 2018 and, at 55% were considerably above the historical average (40%). This rise likely reflects the uptick of reports among the highly regulated Energy, Water & Mining sector, but also within the Property and Retail & Wholesaling sectors, both of which were at record survey highs for the concern this quarter.

Despite strong sales growth, there was an increase in businesses reporting customer demand as a rising challenge and, at 41%, it was marginally ahead of the regional norm (39%) but consistent with the UK average. Competition in the marketplace also edged up to match the historical average (34%).

Investment

At 2.1% in Q4 2025, annual investment growth picked up from a low reported last quarter and businesses intend to maintain growth at that rate next year, marginally ahead of the regional historical norm (2.0%) and stronger than the UK projection (1.6%).

The growth in R&D budgets has been underwhelming in recent quarters in the South West, falling below the regional norm (2.0%) in seven of the last eight quarters. A further deterioration was reported in Q4 2025, with annual R&D budgets contracting by 0.3%, the only region to report a fall in the period, while budgets expanded by 1.6% on average across the UK. The outlook is far more encouraging, with businesses planning growth of 2.6%, the highest rate in the UK and twice the national projection (1.3%).